Finding the right employee health coverage can feel overwhelming for a small business owner. Between rising premiums, ACA compliance rules, and employee expectations, choosing the right provider matters more than ever. That’s where CareFirst small business health insurance enters the conversation.

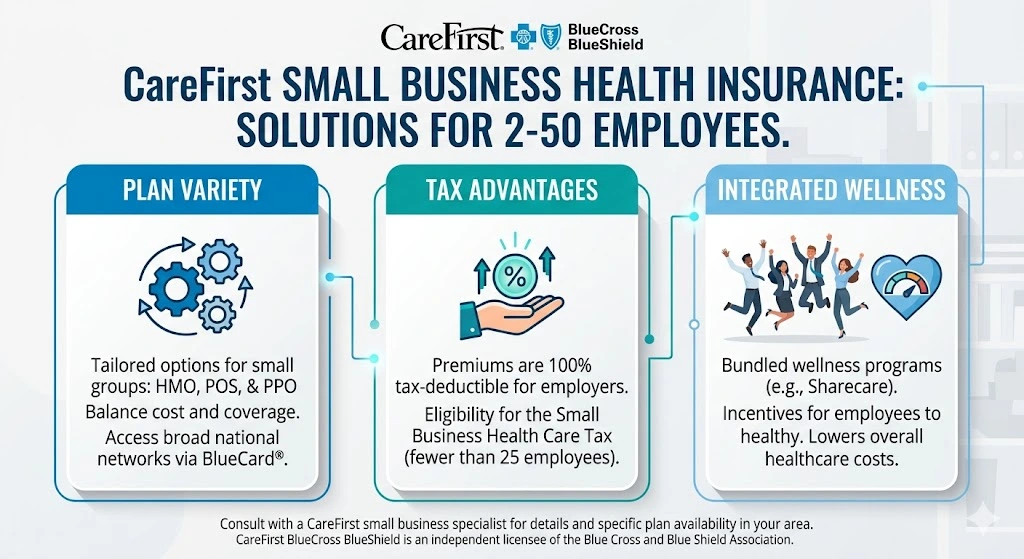

Whether you run a startup with two employees or a growing company with 50 workers, CareFirst offers multiple plan options built around affordability and employee wellness.

In this guide, we’ll break down how CareFirst small business health insurance works, what it covers, estimated costs, advantages, potential drawbacks, and how to decide whether it’s the right fit for your company.

What Is CareFirst Small Business Health Insurance?

CareFirst small business health insurance is a group health coverage solution designed for employers with typically 2–50 employees. These plans help businesses provide medical benefits to workers while complying with Affordable Care Act requirements.

CareFirst operates primarily in:

- Maryland

- Washington, D.C.

- Northern Virginia

As part of the BlueCross BlueShield network, CareFirst gives members access to extensive regional and national provider networks.

Who Qualifies as a Small Business?

Most CareFirst small group plans are intended for businesses with:

- 2 to 50 eligible employees

- At least one full-time W-2 employee besides the owner

- A qualifying business location in CareFirst service areas

Some eligibility requirements may vary by state regulations.

Types of Employer Health Plans Available

CareFirst offers:

- PPO plans

- HMO plans

- High-deductible health plans

- HSA-compatible options

- Dental and vision add-ons

- Pharmacy-integrated coverage

This flexibility allows employers to balance monthly premiums with employee healthcare needs.

Why Small Businesses Choose CareFirst

Small businesses often choose CareFirst because it combines broad healthcare access with recognizable BlueCross BlueShield branding.

Large Provider Network

One of CareFirst’s biggest selling points is its network access. Employees can often choose from:

- Large hospital systems

- Regional specialists

- Primary care physicians

- Nationwide BlueCard provider access

For businesses with remote or traveling employees, this can be a major advantage.

Employee Retention and Recruitment

Health benefits remain one of the most valued employee perks. Competitive insurance helps businesses:

- Attract stronger candidates

- Improve retention

- Reduce turnover costs

- Increase workplace satisfaction

Many employees consider healthcare benefits nearly as important as salary.

Wellness and Telehealth Benefits

CareFirst plans often include:

- Virtual doctor visits

- Mental health support

- Wellness incentives

- Nurse advice lines

- Preventive care services

Telehealth access has become especially important for busy employees who want faster care without visiting a clinic.

Tax Advantages for Employers

Employer-sponsored health insurance can offer tax benefits, including:

- Tax-deductible premium contributions

- Reduced payroll taxes

- Potential small business healthcare tax credits

For many businesses, these tax savings partially offset insurance costs.

What Does CareFirst Small Business Insurance Cover?

Coverage varies by plan, but most ACA-compliant CareFirst plans include essential health benefits.

Preventive Care

Preventive services are commonly covered at no additional cost, including:

- Annual wellness exams

- Vaccinations

- Blood pressure screenings

- Routine preventive tests

Preventive care helps employees stay healthier and can reduce long-term claims costs.

Prescription Drug Coverage

Most plans include integrated pharmacy benefits covering:

- Generic medications

- Brand-name drugs

- Specialty prescriptions

- Mail-order pharmacy options

Prescription tiers and copays vary by plan level.

Mental Health and Telehealth

Mental health coverage has become increasingly important for employers. CareFirst commonly includes:

- Behavioral health support

- Virtual therapy access

- Stress management programs

- Online mental wellness tools

Dental and Vision Add-Ons

Employers can often bundle:

- Dental insurance

- Vision coverage

- Orthodontic options

- Annual eye exams

Bundled benefits can create a more competitive employee package.

CareFirst Plan Types for Small Employers

Choosing the right plan structure is critical because it directly impacts monthly costs and employee satisfaction.

PPO Plans

Preferred Provider Organization (PPO) plans offer:

- Greater provider flexibility

- Out-of-network options

- Specialist access without referrals

PPOs are usually more expensive but highly popular among employees.

HMO Plans

Health Maintenance Organization (HMO) plans typically:

- Cost less monthly

- Require in-network care

- Use primary care referrals

HMOs can work well for budget-conscious businesses.

High-Deductible Health Plans (HDHP)

HDHPs feature:

- Lower premiums

- Higher deductibles

- Eligibility for Health Savings Accounts

These plans appeal to younger or healthier employee groups.

HSA-Compatible Plans

HSA plans allow employees to:

- Save pre-tax money for healthcare

- Build long-term medical savings

- Reduce taxable income

Many employers contribute to employee HSAs as an added benefit.

How Much Does CareFirst Small Business Health Insurance Cost?

There’s no universal pricing because multiple factors influence premiums.

Factors That Affect Pricing

Key pricing variables include:

- Employee ages

- Business location

- Plan type

- Deductible level

- Employer contribution percentage

- Number of enrolled employees

Generally, richer coverage means higher monthly premiums.

Employer Contribution Requirements

Most group plans require employers to contribute a minimum percentage toward employee premiums.

Many businesses contribute:

- 50% to 80% of employee-only coverage

- Optional dependent contributions

Higher employer contributions usually improve employee participation.

Ways to Reduce Premium Costs

Businesses often lower costs by:

- Choosing HDHP plans

- Offering wellness incentives

- Using level-funded arrangements

- Encouraging preventive care

- Working with experienced brokers

Even small plan design changes can create meaningful savings.

CareFirst vs Other Small Business Health Insurance Providers

Comparing insurers is important before making a final decision.

| Feature | CareFirst | Typical Regional Insurer |

| Provider Network | Large BCBS access | Often smaller |

| Telehealth | Included in many plans | Varies |

| Wellness Tools | Strong offerings | Moderate |

| Brand Recognition | High | Moderate |

| ACA Compliance | Yes | Usually |

| National Access | Strong | Limited |

Network Comparison

CareFirst’s BlueCross BlueShield affiliation gives employees broader provider access compared to many local carriers.

Digital Tools and Member Experience

CareFirst offers:

- Online portals

- Mobile account management

- Digital ID cards

- Claims tracking

However, some users report occasional website or customer service frustrations during high-volume periods.

Customer Support and Claims Experience

Experiences vary depending on:

- Plan type

- Broker support

- Local provider coordination

Working with an experienced broker often improves the overall enrollment and support process.

How to Enroll in a CareFirst Small Business Plan

Enrollment is typically straightforward when documentation is prepared in advance.

Required Documents

Businesses may need:

- Employee census data

- Tax documentation

- Business license information

- Payroll records

Enrollment Timeline

Many employers begin shopping:

- 30–60 days before coverage starts

- During annual renewal periods

- After major hiring growth

Working With a Broker

Insurance brokers can help:

- Compare plans

- Explain pricing

- Handle paperwork

- Negotiate renewal options

For small employers, broker guidance often simplifies the process significantly.

Is CareFirst Small Business Insurance Worth It?

For many Mid-Atlantic businesses, CareFirst provides a solid combination of network size, ACA compliance, and flexible plan design.

It may be a strong fit if:

- Your employees want broad provider access

- You need multiple plan options

- You value BlueCross BlueShield branding

- You want integrated wellness benefits

However, businesses should still compare:

- Monthly premiums

- Deductibles

- Network restrictions

- Customer support quality

The best health insurance plan depends on both employer budget and employee healthcare priorities.

Frequently Asked Questions About CareFirst Small Business Health Insurance

How many employees do I need for CareFirst small business health insurance?

Most CareFirst small group plans require at least 2 eligible employees, though exact rules vary by state.

Does CareFirst offer ACA-compliant small business plans?

Yes. CareFirst small business plans are generally ACA-compliant and include essential health benefits.

Can employees use CareFirst coverage outside Maryland or D.C.?

Many PPO plans include nationwide BlueCross BlueShield network access, allowing broader provider usage.

Does CareFirst include telehealth services?

Yes. Many plans include virtual healthcare services, mental health support, and nurse advice lines.

Are dental and vision benefits available?

Yes. Employers can often add dental and vision coverage to their group benefits package.

Is CareFirst good for startups?

CareFirst can work well for startups needing flexible group coverage, especially in Maryland, D.C., and Northern Virginia.