What increases your total loan balance even when you’re doing everything “right”?You make payments. You stay on schedule. Yet your loan balance refuses to fall, or worse, it slowly climbs. This isn’t carelessness. It’s design. Loans are built in a way that allows interest, fees, and timing to silently push your balance higher if you don’t understand the rules. Most borrowers never see it happening until the cost becomes painful.

This guide explains exactly what increases your total loan balance, why it happens, and how to stop losing money you don’t need to lose.

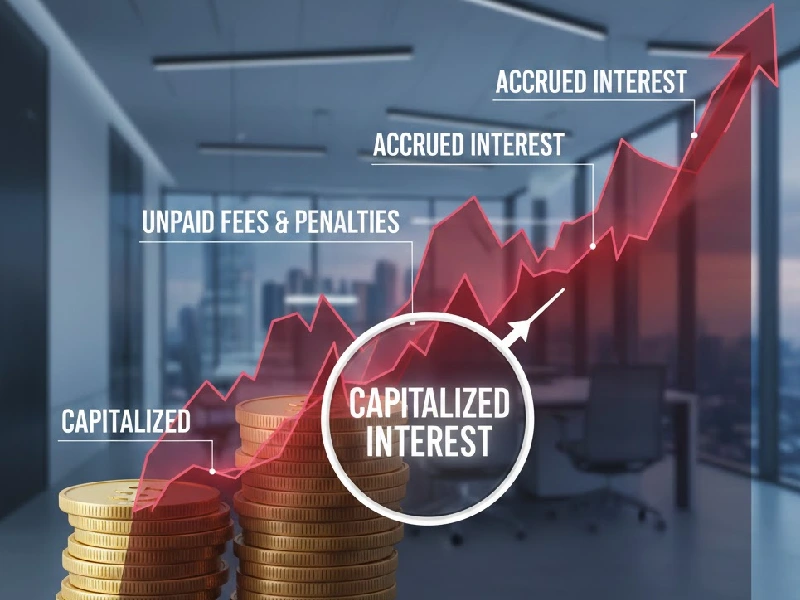

What Is a Total Loan Balance? (The Part Most Borrowers Miss)

Your total loan balance is not just the amount you originally borrowed. That’s where most confusion starts.

A typical loan balance includes:

-

Remaining principal

-

Accrued interest

-

Unpaid fees and penalties

-

Capitalized interest added later

That’s why your balance can increase without taking another dollar.

Understanding this single concept makes everything else clearer.

What Increases Your Total Loan Balance the Most?

Direct answer:

Interest accrual, capitalized interest, unpaid fees, minimum payments, and payment pauses are the biggest reasons your total loan balance increases.

These factors work quietly. Separately, they seem small. Together they compound fast.

Let’s break them down.

How Interest Slowly but Constantly Increases Your Loan Balance

Interest is the primary engine behind rising loan balances.

Many borrowers assume interest is applied monthly. In reality, most loans calculate interest daily.

That means:

-

Your balance grows every day

-

Payments cover interest first

-

Principal reduction comes later

Even one delayed payment allows interest to gain ground.

Simple Interest vs Compounding Impact

Some loans use simple interest. Others allow interest to compound indirectly through capitalization. Either way, interest favors time — and lenders know it.

The longer your balance stays high, the more interest you pay.

Capitalized Interest: The Hidden Balance Accelerator

Capitalized interest is one of the most expensive surprises borrowers face.

It happens when unpaid interest gets added to your principal. Once that happens, future interest is calculated on a larger base.

Common situations where interest capitalizes:

-

Student loan deferment

-

Forbearance

-

Loan consolidation

-

Certain refinance scenarios

This is why balances often jump suddenly after a pause in payments.

You didn’t borrow more. The math changed.

Fees and Penalties That Quietly Increase Your Loan Balance

Fees feel minor. Over time, they’re not.

Common fees that raise balances:

-

Late payment fees

-

Origination fees

-

Administrative or servicing charges

-

Collection-related penalties

If fees aren’t paid immediately, they often get added to your balance. Once that happens, interest applies to them too.

That’s how small mistakes turn into long-term costs.

Minimum Payments: Why Paying “On Time” Isn’t Always Enough

This is one of the most misunderstood parts of borrowing.

Minimum payments are designed to:

-

Keep you current

-

Extend repayment

-

Maximize interest revenue

In some loans, the minimum payment doesn’t fully cover interest. The unpaid portion gets added back to the balance.

This process is called negative amortization.

Loans Where This Commonly Happens

-

Credit cards

-

Adjustable-rate loans

-

Income-based repayment plans

You’re paying — but not enough to move forward.

Deferment and Forbearance: Short-Term Relief, Long-Term Cost

Deferment and forbearance can feel like lifesavers when money is tight. But they’re not free.

During these periods:

-

Payments pause

-

Interest usually continues accruing

-

Interest may laterbe capitalizede

When repayment resumes, borrowers often face a larger balance than before, even though they didn’t miss a payment.

It’s relief now — with a price later.

Missed or Late Payments: How One Slip Increases Total Debt

Missing payments doesn’t just hurt your credit. It directly increases your loan balance.

Here’s what typically happens:

-

Late fees are added

-

Interest continues accumulating

-

Penalty terms may apply

The longer a payment stays overdue, the faster the balance grows. One missed payment can snowball into months of extra cost.

Refinancing a Loan: Can It Increase Your Balance?

Refinancing often sounds smart — and sometimes it is. But it can also raise your balance quietly.

Your balance may increase if:

-

Unpaid interest is capitalized

-

Fees are rolled into the new loan

-

The repayment term extends significantly

Lower monthly payments don’t automatically mean lower total cost.

Always look at the new starting balance, not just the monthly number.

Real-Life Examples of What Increases Your Total Loan Balance

Personal Loan Example

-

Borrowed: $6,000

-

Entered forbearance for 5 months

-

Interest capitalized afterward

-

New balance: $6,500+

Student Loan Example

-

Interest accrued during school

-

Capitalized at graduation

-

Balance increased before the first payment

Auto Loan Example

-

Missed two payments

-

Late fees added

-

Loan term extended

-

The total cost increased significantly

These aren’t rare cases. They’re common outcomes of normal loan features.

Psychological Traps That Keep Balances High

Beyond math, behavior matters.

Common borrower traps:

-

Only paying the minimum

-

Avoiding statements

-

Using deferment too often

-

Refinancing without comparing totals

-

Ignoring interest during pauses

Loans reward awareness. They punish autopilot.

How to Stop Your Total Loan Balance From Increasing

You can’t remove interest entirely. But you can control how much power it has.

Proven strategies that work:

-

Pay more than the minimum whenever possible

-

Make interest-only payments during deferment

-

Avoid long forbearance periods

-

Pay on time, every time

-

Review statements monthly

-

Ask lenders how interest is applied

-

Refinance only when numbers make sense

Small changes consistently applied create major savings over time.

How Long Does It Take for Balances to Shrink Faster

Once your payments exceed interest:

-

Principal drops faster

-

Interest costs fall

-

Momentum builds

This is the turning point borrowers feel.

Until then, balances move slowly. After that, progress accelerates.

Key Takeaways: What Increases Your Total Loan Balance

Your loan balance grows because:

-

Interest accrues daily

-

Capitalized interest increases principal

-

Fees and penalties add up

-

Minimum payments stall progress

-

Payment pauses aren’t free

Understanding these rules changes everything.

When you know what’s working against you, you stop overpaying — and start winning.

Frequently Asked Questions (FAQ)

What increases your total loan balance even when you pay every month?

Interest accrual, capitalized charges, and minimum payments can silently increase your balance despite consistent payments.

Why does my loan balance go up instead of down?

Because interest and unpaid charges may exceed the amount your payment reduces fromthe principall.

Does deferment increase your total loan balance?

Yes. Interest usually continues accruing and may later be added to your principal.

Why does refinancing sometimes increase loan debt?

Fees and capitalized interest can raise the new loan’s starting balance.

What’s the fastest way to stop my loan balance from growing?

Pay more than the minimum, reduce interest exposure, and avoid unnecessary payment pauses.